Money is losing Value

Hi Money makers,

Welcome to TalkingCents, a weekly newsletter about finance, investment, and economics. If you’d like to learn more and be part of the community, then you can join by clicking here.

In today’s article I’m going to be talking about the Time Value of Money and how your youth is being stolen from you.

Time Value of Money

This is a financial concept that is extremely misunderstood and hard to conceptualize, but I am going to explain it to you in the easiest way possible. Once understood, you will realize the importance and necessity of investing and protecting your economic output. (energy)

The Time Value of Money (TVM) explains how money is worth more today than the same sum will be at a future date.

For example:

A R100 today won’t be worth R100 next year, because the same amount will buy you less.

Many of us refer to this as inflation,

meaning the prices of everyday things increase, but as a matter of fact, the price of things are not increasing, rather it is the value of money that is diminishing.

If you were to measure the price of milk in something else other than the Rand, let’s say gold, then you’d see that the price of milk against gold would have been relatively the same over the years. But when measured in currency (Rand) we see that prices are forever increasing.

This is why going forward you shouldn’t think about inflation as ‘prices going up’, but rather as the ‘value of your money going down’.

This applies to all currencies,

whether it is the Rand, Dollar or Pound, all of them lose value in the same way as described above, just some lose value more quickly than others.

Because you now know this,

then you can understand that inflation is the primary reason for this destruction in purchasing power over time. It can be used to express how Time Value of Money exists.

Money upfront or Money in installments

If someone owes you money and promises to pay you back,

then ideally you should always take the upfront money now rather than being paid off in installments because they are paying you back with money that is worth less in the future. (especially if you aren’t charging them interest)

Now you can understand why banks charge you interest on money they lend to you, otherwise it would be a transfer of wealth.

It would be a transfer of wealth from the person lending the money to the person who borrows the money. Therefore, banks and other financial institutions charge interest because of the time value of money, in order for them not to lose value.

You can’t borrow R1 million and then expect to pay back only R1 million, because R1 million in the future would probably only be worth R900 000.

The bank would then be losing money if they didn’t charge you interest on the borrowed principal. If they didn’t charge you, then they would be transferring their wealth to you the borrower. (You’ll see why shortly)

Let me explain this further,

I’m going to break it down into 3 simple things:

(1) Opportunity cost

(2) Present moment

(3) Investments

1. Opportunity cost

An opportunity cost is the value lost over choosing one option over another, It is considered to be an unseen cost.

By not receiving your money today, then there is an opportunity cost of receiving that money on a date in the future, as opposed of today.

Banks know this,

so they must be compensated for this value destruction of future purchasing power, hence they charge interest. (to keep up with the pace of value destruction).

Example

If you received R100 000 today,

you can immediately invest that money if you wanted to. However, If that same amount of money is received 5 years from now instead, then the 5 years of waiting for it represents the opportunity cost that has been lost. (because you could have invested the money and earned a return on it.)

Here is a detailed explanation of what an opportunity cost means.

2. Present moment

Money available today could be invested immediately into something that can generate a return for you. (Yield) By waiting for money to be paid to you, you lose the opportunity of earning from or on it.

Take this example:

If someone owes you R10 000, then that money could have been invested at 10% per annum. After 1 year you would have had R11 000.

(R10 000/100 *10 = R1 000 )

This simply means, that R11 000 a year from now is essentially equivalent to R10 000 in today’s money.

If that person gives you back the R10 000 they owe you one year later, then the opportunity cost of not investing would have been 10% because that’s the rate you could have invested the money if you hadn’t lent it out to them.

If they only give you R10 000 back in a year from now, then that would be worth R9 000 in today’s money, because you missed the opportunity to invest it, and money continually loses value. (basically they underpaid you)

Therefore, by not charging interest on money that is owed to you, you transfer your wealth to the borrower, because they pay you back with money worth less in the future. (that’s why banks charge interest)

3. Investments

Provide investors with guaranteed interest on their capital, which compounds over time.

For example:

•Fixed deposit accounts

•Dividend stocks

Because of this, we know that time has a direct and easily calculated impact on the value of money, since some monetary growth (gains from investments) can easily be realized with your R10 000 right now, and it can be earned ‘essentially’ free of risk.

This is why money right now is generally worth more when it's received sooner than later.

Value destruction

I want to drive this point further of how money loses value over time, so I will take you back to the early 1980’s when milk costed R1.72 for 2 liters.

Said differently,

86c was worth the price of one liter of milk at that time. However, today 86c is worth much less than a liter of milk.

In fact, the price of one litre of milk today is easily around the R12.50 range. Remember, it’s not the price of things going up, its ‘your money losing value’

Just Imagine you were still waiting for your 86c from someone that owed you money in the 1980’s. If you had gotten your 86c back then, then you would have still been able to buy your milk.

However, if they had only paid you your 86c today (2022), then your 86c wouldn’t be able to buy you milk anymore. (Do you see that transfer of wealth if you wait for your money) - they paid you back with money that is worth much less.

This is why money held many decades ago was worth more than it is now, because you were able to buy more with the money in the past than you are able to today, and this will be the case 30 years from today too.

Here are more examples below of what things costed in the 1980’s.

This is why it’s important to put your money to work and invest it into assets that make your money grow over time, because if you don’t, your salary just won’t suffice.

Protecting Wealth

When the growth portion of an investment itself begins to increase in value over time, this is called compounding, and this is why time has a major impact in the value of our money.

The system has been designed to rob those who don’t understand it. This is why it is super important to spend less than you earn each month and invest the difference, because your salary will always keep you trapped in this system. It is why you feel as if you are never winning, because you literally aren’t.

One must own assets that generate cashflow, so that you can continue to produce money in the future, in order to maintain your purchasing power.

Now we can understand Einstein a bit better when he says:

Calculations

Here are the main variables in the time value of money formula, which can be used to calculate the rate at which your money is expected to grow:

• FV = Future value of money

• PV = Present value of money

• i = interest rate

• n = number of compounding periods per year

• t = number of years

You can also use online calculators for this if you are not a fan of the math.

Example

To calculate the future value of money based on the present value

FV = PV x (1+i)n

R100 000 at 8% for 10 years which will be compounded 1 time in the year.

= R 215 892.50

This means that the future value (10 years from now) of R100 000 will be R215 892.50

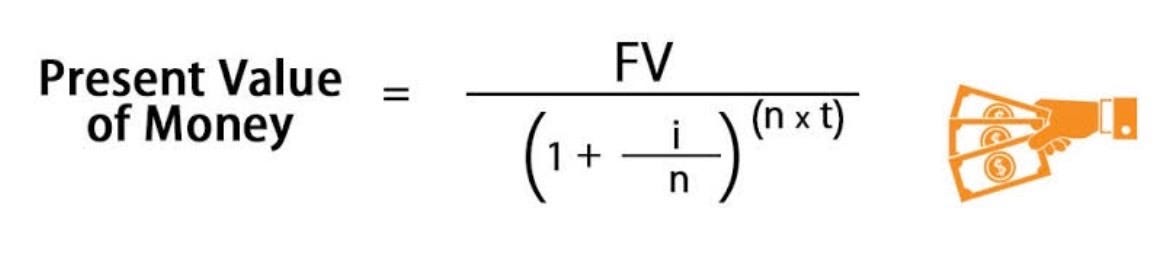

One can also calculate the present value of a future sum:

PV = FV/(1 + i)n

R215 892.50 ÷((1.08)10)

= R100 000

This means that R215 892 in the future is equivalent to R100 000 in today’s money.

The best way to understand TVM is with a time value of money example that shows how much investment growth is capable over time with compound interest.

Let’s take R100 000 and invest it into an account, bond, or annuity that compounds annually with a rate of return of 8%

These are the amounts that would reflect in your account after each period:

R108,000 in year 1

R125 971 in year 3

R146 932 in year 5

R215 892 in year 10

R466 095 in year 20

R684 847 in year 25

Takeaway:

The longer money is invested, the faster it grows due to compound interest.

Making investment Decisions

Quantifying the time value of money via a TVM calculation is crucial for financial planning and for doing business.

It is also a key part of a discounted cash flow analysis (DCF) which is a popular way to determine the future value of invested money.

You really shouldn’t be investing money without knowing these formulas, because you could be essentially overpaying in the current moment for an asset that won’t yield significant growth in the future.

This is why it is so dangerous buying a stock that is hyped, or property that is overvalued, because your money won’t be put to good use, and the opportunity cost of being invested may be detrimental to your overall net worth.

Here is a detailed thread on how to value companies or businesses, so you don’t end up overpaying.

Closing thoughts

The time value of money is an important concept for understanding the impact of time on the value of money, predicting how much individuals and companies need to invest to meet future goals, and calculating the future value of investments.

When allocating capital, you want to know that you are putting it to good use, and you want to ensure you are protecting yourself from this corrupt system.

These weren’t the things we were taught in school, but luckily for you, you have subscribed to TalkingCents.

I’d like to urge you all to forward this to your closest friends and family members, so that we can start educating those around us about how the system works.

The sooner we do that, the sooner we can stop being taken advantage of.

Stay safe, everyone

See you next week :)