Amortization

Hi Money makers,

I’ve been away from my weekly newsletters for a few months now, but I haven’t forgotten about you.

I’ve been working on content that is educational and informative for you to consume. Over the next several weeks you can expect to receive more of the same quality you have gotten used to - absolutely FREE!

If this is your first time here,

welcome to TalkingCents, this is a weekly newsletter about finance, investment, and economics. If you’d like to be part of this community, then you can join by clicking here.

In today’s article I’m going to be talking about the two forms of Amortization.

What is Amortization?

The term “amortization” refers to two different situations:

First:

It is used in the process of paying off debt through regular principal and interest payments over time. (think of a home loan)

Second:

Amortization can also refer to the practice of spreading out capital expenses related to intangible assets over a specific duration. (lifetime of that asset).

The second definition is more accounting and business focused, therefore I will be focusing mainly on definition (1) because most of you are possibly homeowners or potentially looking to be in the future, and definition (1) focuses on debt, mainly debt needed to buy property.

Let’s take a look at what I mean.

Why does debt never seem to go down

When buying property,

you predominately use someone else’s capital, the bank’s capital, mainly because you don’t have the full amount needed to buy the asset (property) in cash.

Therefore, you are going to take on debt, which is backed by the asset and your ability to repay. (We call this asset financing).

What this means is that the bank is taking the risk of lending money to you, and because you don’t have the full amount needed to make the purchase, they (the lender) will charge you a fee, also known as interest.

When you borrow money from the bank, we call that the principal, and the cost for borrowing that money is called the interest.

The set date at which principal and interest must be paid back in full is called the maturity date. (principal + Interest )

Amortization Explained:

“It is the process whereby a loan is paid off by paying the amount of principal plus the amount of interest in a specific time”.

As you make your payments to the lender for the purchase of your property, you begin to pay off your loan over its term. Each month you make the minimum payment required and you go on with your life.

However, this is the part where confusion arises and where many of us neglect our finances.

Each monthly payment is broken off into two parts:

1. Interest payment – which goes to the lender (your bank). This is the fee they take for lending you the money to be a ‘property owner’

2. Principal payment – Which goes towards paying down your bond. (Loan amount)

*Your interest portion of your payment is calculated based on your loan interest agreement (interest rate you signed at) and the remaining balance of your loan.

*The principal payment amount is what remains after the interest portion has been deducted from your monthly payment.

Interest vs Principle

There is an inherent risk when lending money to strangers, so banks want to be compensated for this risk, and how they do it, is that they pay themselves first.

While your total monthly payment stays the same from month to month, it’s your interest and principal portions that change in size over time.

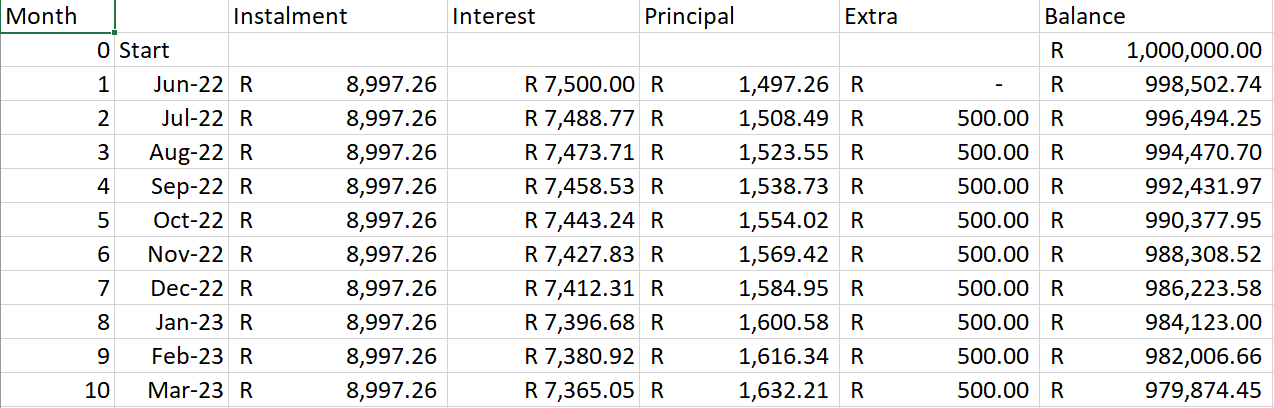

For example:

A bond of R1 million @ 9% for 20 years

The full monthly payment for your loan would be R8997.26

R8997.26 is the amount you would pay every month which would then be broken down into two payments:

1. Interest (R7 500)

2. Principal (R1 497.26)

To work out the interest portion you’d pay,

you would simply multiply the principal amount by the interest amount (0.09) then divide by the number of months in a year.

( R1million x 0.09 ) ÷ 12 = R7 500

When your lender receives your full amortization payment, the first thing they do is pay themselves in the amount equal to the interest portion. (R7 500)

Then your principal contribution is what remains after the lender has paid themselves the interest portion.

( R8 997.26 - R7 500 = R1 497.26 )

After that, the lender will then reduce your loan balance by your left-over principal payment.

(R1million - R1 497.26 = R998 502.74 )

When you make your payment again in month two,

your new loan balance of R998 502.74 will now be used to calculate the interest portion of your fully amortized payment.

That means you would now owe a smaller amount to the lender in the form of interest in month two because your loan balance amount has been reduced slightly.

( R998 502.74 x 0.09 ) ÷ 12 = R7 488.77

Your interest charge for month two will be lower because the loan balance is lower.

This process repeats itself each month, with the interest portion amount gradually declining and the principal portion gradually rising.

Every month that this goes by, you are paying less and less interest because your loan balance is lower each month.

After 10 months,

you have paid R89 972.60 in monthly payments

but only R15 488.16 has been taken off your loan balance (your debt).

Additional contributions

One way to accelerate this process is to pay extra towards your bond each month. In fact, it is crucial to do so in this rising rate environment we find ourselves in. Simply because there is a cost to capital (the price you pay for the money you borrowed).

All extra payments you are able to make become 100% principal, meaning they go straight to paying down the loan amount. Even small extra payments can have a large positive effect on your finances in the long term.

Making extra payments saves you money because it reduces your interest expense, which is especially important now if rates do continue to rise. (which they will)

Just look at your savings, and this compounds in the long run.

Think of these extra payments as an investment that earns you a guaranteed return on capital equal to your loan interest rate (9% in our example)

You may even find it more beneficial to redirect extra money into paying down your bond quicker, because those savings can potentially earn you a yield that outperforms other alternative investments.

WRAP UP (definition 1)

Schedule (the amount of time needed to pay back the loan)

Interest (cost of borrowing)

Principal (amount borrowed)

Property isn’t something you rush off into because it will require massive amounts of capital to be sustained.

South Africans have been lead to believe that property is the best investment one can make, and maybe this was the case 20-30 years ago, but it’s simply not true now in our current environment.

This is because asset prices have risen faster than real wage growth over the years, and inflationary pressure can no longer be passed onto tenants.

With that being said, it’s not all doom and gloom. There is an intangible and unquantifiable value associated with owning a home that one cannot calculate - it brings peace of mind, security for your kids, and a place that’s your sanctuary, and some things are worth paying a premium for.

The best tip I can give you is that it is a good idea to speed up the process and pay extra into your bond whenever you can. This will pay down the loan balance quicker and save you money in the long run.

PAY EXTRA NOW TO SAVE LATER.

Quick side note:

There are many good deals out there at the moment, but not many who know how to source them, don’t run in blindly, especially if you have a business and want to buy property to conduct commercial activities. If you have a business and need to buy property, then I’d suggest reading this article first

Definition 2

Amortization and Depreciation

In this section,

I will briefly explain what amortization means when it comes to doing business and spreading those capital payments out.

Before we look at what it exactly entails, we need to make a differentiation between amortization and depreciation.

They are both similar concepts, in that both attempt to capture the cost of holding an asset over time.

𝘼𝙈𝙊𝙍𝙏𝙄𝙕𝘼𝙏𝙄𝙊𝙉 and 𝘿𝙀𝙋𝙍𝙀𝘾𝙄𝘼𝙏𝙄𝙊𝙉

Here, amortization refers to intangible assets. (things you cannot touch)

𝙀𝙭𝙖𝙢𝙥𝙡𝙚𝙨:

•Trademarks

•Patents

•Copyrights

Depreciation refers to tangible assets (things you can touch)

𝙀𝙭𝙖𝙢𝙥𝙡𝙚𝙨:

•Equipment

•Buildings

•Vehicles

𝘼𝙈𝙊𝙍𝙏𝙄𝙕𝘼𝙏𝙄𝙊𝙉 Explained

Simply put,

It measures the consumption of the value of an intangible asset.

When businesses amortize intangible assets over time, they are able to tie the cost of those assets with the revenue generated over each accounting period. This allows the company to benefit from the use of a long-term asset over a number of years.

Therefore,

it writes off the expense incrementally over the useful life of that asset.

For example:

Company XYZ purchased an intangible asset for R100 000 with a lifespan of 10 years. They then amortized the expense for this R100 000 intangible asset. Which then results in R10 000 a year.

Is Amortization Important?

It’s important because it helps businesses and/or investors to understand and forecast their costs over time.

Amortizing intangible assets can reduce a business's taxable income, while giving investors a better understanding of the company’s true earnings.

I will keep this second definition of amortization short and stop here, because the main focus is on definition (1), which I believe has a more direct impact in our everyday lives.

SUMMARY

There are two forms of amortization:

1. Paying off debt

2. Spreading capital expenses

In the context of loan repayment,

amortization schedules provide clarity into what portion of a loan payment consists of interest versus principal, this can be useful for purposes such as deducting interest payments for tax purposes.

Feel free to watch this video that explains the above concepts in video format.

It’s good to be back, please feel free to reach out to me if you have any feedback.

Until then…

Stay safe, everyone

See you next week :)