Earn 11% Risk-Free

Hi Money makers,

Welcome to TalkingCents, a weekly newsletter about finance, investment, and economics. If you’d like to learn more and be part of the community, then you can join by clicking here.

In today’s article I’m going to be unpacking how you can earn 11% with little to no risk with South African Retail Savings Bonds

Before we get started,

There are two things you will learn about today:

What bonds are

What their functions are

* when we talk about bonds in this article we are not talking about money owed to the bank for your property. (It’s why Americans call it a mortgage)

Companies and Governments

A bond is a debt security, think of it as an IOU. You lend money to someone, and then they promise to pay you that money back + sum, known as interest.

Companies and governments can both issue bonds to raise capital for their capital needs, future expenditures, or for investment purposes.

In this article we will be looking at government bonds.

A government bond is a debt security that is issued by a government to support government spending and their obligations. If a government is in need of capital, they issue bonds in exchange for an investor’s capital, this investor is then compensated in the form of interest payments (coupon payments) for lending their money to the government. Read more here

RSA Retail Savings Bond

An RSA Retail Savings Bond is an investment with the Government of South Africa which earns fixed or inflation linked interest for the term of the investment.

- No fees

- No commission

- No Risk (So they say)

- Guaranteed returns

There are 3 types of bonds you can opt for:

• Fixed Term

• Inflation-linked Bonds

• Top-up Bond

Let me explain each one:

(1) Fixed Term

The fixed term option is very similar to a fixed deposit at a bank account. It is when you lock your money up for a certain period without having access to it. Either for 2 years, 3 years, or 5 years.

Just as if you would give your money to the bank, you’d be giving your money to government instead. Both will offer you a set rate of interest for borrowing your money.

The longer the term you stay locked up for, the higher the interest rate will be. They (banks or government) will use your money either for investment purposes, or in the case of government, to possibly fund their deficits.

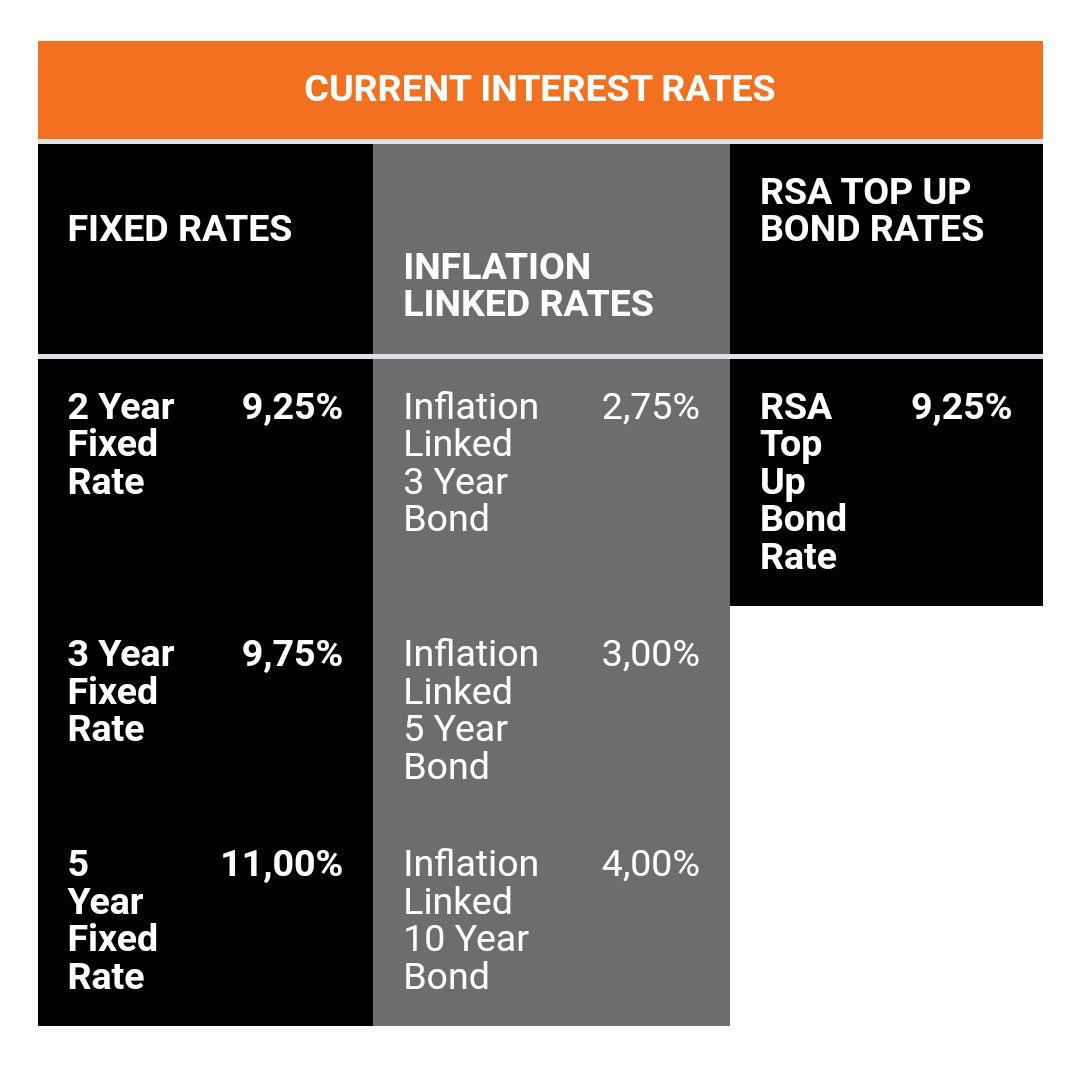

Here are the fixed rates for RSA Retail Savings Bonds:

2 year = 9.25%

3 year = 9.75%

5 year = 11%

(2) Inflation-linked Bonds

You earn a certain % above the inflation rate, known as 'the real local return’. To work out your local real return, you would simple take the

(The interest rate you’ve invested at - inflation rate)

For example:

Inflation = 7%

Fixed interest rate = 6%

(6%-7%) = (-1%)

in this case, your real local return would be negative (you are losing purchasing power).

You can see now why interest rates are going up, to bring down inflation and to move rates into positive territory.

I won’t focus on how rising rates affects other asset classes in this environment, but I promise to touch on it in future articles.

Let’s get back to RSA Retail Savings Bonds, here are the rates for inflation linked bonds:

3 year = 2.75%

5 year = 3%

10 year = 4%

*(remember, these returns are above inflation, that means inflation + % rate on offer) For a 3 year, you’ll earn 2.75% above what the current inflation rate is. This is to ensure you don’t have a negative real return like in the example above.

(3) Top-up Bond

This is a newly introduced option to encourage savers.

Prior to this option,

you needed a minimum of R1 000.00 to invest into bonds and you couldn’t top up on the existing bond you had, you would have needed to get a new bond each time.

at the present moment,

you can now invest into top-up bonds with as little as R100.00 and you can add to it when you want without the need to buy a new bond each time.

This bond option has no fixed-term and you can add to it when you like. However, interest rates fluctuate as they reset each month.

Current Rate = 9.25%

Key Takeaways

With all three options,

the rate on offer resets on a monthly basis, so the current rate of 11% for August may not be on offer again next month. The last time it was this high was in 2020.

If you opt for option (1) or (2) you will lock in the current rate that is on offer for the respective time period, and it won’t fluctuate going forward.

That simply means that if you lock in 11% for 5 years, you can expect that rate even if the rates subsequently drop. And if the rates rise higher, you have the option of restarting your investment at a higher rate, but then you’d be locking your funds up again as if you had just bought new bonds.

For example:

If you lock in 11% for 5 years and after year 3 the rate jumps to 14%, you can then restart your investment at the higher rate of 14%, but then you’d have to wait 5 years again to access your money and not two years anymore.

Government Bonds

There are many different types of bonds that are traded on the primary and secondary markets. RSA Retail Savings Bonds are traded on the primary market, whereas government bonds are traded on the secondary market.

RSA Retail Savings Bonds derive their value (current rate on offer) from government bonds on the secondary market. The repo and prime rates don’t dictate the rate on offer for the RSA Retail Savings Bond.

The RSA Retail Savings Bond rate tracks the movement of the government’s bond rate in the secondary market.

Usually, if government bond yields rise (debt more expensive) then yields on the RSA Retail Savings Bonds have to adjust upwards too. This is why RSA Retail Savings Bonds reset on a monthly basis, because they track government bonds in the secondary market.

Bonds and yields in the secondary market track the risk associated with investing in South Africa, which then affects currency. A higher yield means people are selling S.A bonds because it’s considered riskier, hence government must offer higher rates on bonds to attract capital.

You can track the bond prices and their yields to get an idea of how interest rates will adjust and to gauge the direction of the currency (ZAR)

Remember,

in a crisis these yields will rise and bonds will move lower because no one wants to be holding debt of an emerging market country when there is a crisis.

Bonds and yields move inversely to each other.

If people buy bonds, then the yields go down because they trust the country, + vice versa. If bonds drop in price then yields will rise because no one wants to buy the debt, and rates must move higher to try attract that capital.

In the picture below are the the bonds in the secondary market that dictate the rate of RSA Retail Savings Bonds.

These bonds are debt and they reflect risk appetite for South Africa.

If you are feeling confused at this stage, then I’d highly recommend reading this article to understand what I am talking about. Click here

Risks For Retail Savings Bonds

Earlier I mentioned that there is no risk.

Well…… this is not true, this is just what it says on their website. I’ll share with you the real risks that people don’t know about.

Let’s break it down,

Because RSA retail savings bonds are bought in the primary market and the government is backing them (promising to pay you back). Your capital is guaranteed.

sounds great, right? But wait…….

There are two reasons why this is a lower-risk investment option and why the government isn’t likely to not pay you your money back.

(1) Retail Savings Bonds only make up a small percentage of the overall government debt, so their liability is smaller.

(2) Government owns the printing press, they can just print you your return.

HOLD THE F*** UP!!

Did you just say print me my return?

Yes, you heard me correctly! The nominal value of your investment goes up by the % they have promised, that’s true, but that doesn’t mean that’s what you really get.

There is a big difference between nominal returns and real returns

Check this very important thread out to understand what I mean

The risks can be broken down into four simple to understand points:

1. Rand trajectory

2. Inflation rate

3. Tax consequences

4. Opportunity costs

(1) Rand Trajectory (Rand Depreciation )

If the Rand is going to depreciate further, then real returns benchmarked against the dollar will probably be much lower.

The government cannot default on its debt, it can just print you what it promised. However, this would lead to currency depreciation.

For example:

If you invest R100 000.00 at 11% for 5 years.

After 5 years you’d have R170 934.14 (70.93%) = 14.18% each year (that’s damn attractive, folks)

But let’s assume you have no more faith left in the state, and the Rand depreciates from its current levels of R16 to R25 to the dollar in 5 years time while your money is locked away with the government. That’s a massive 36% depreciation in the currency. Although your R100k is now worth R170k, what you are able to buy will be a lot less because of the currency depreciation.

I’m not saying this is what is going to happen, I’m just pointing out that that is a risk. There is a risk of the currency depreciating and in interest rate parity.

Remember,

South Africa is a net importer and commodities are traded in dollars, so the cost of energy and other important commodities you need for everyday life will move up higher (cost more) because of the deprecation of the currency.

Here is the formula you need to work out real returns

Y = local return ( 70.93% ), the return from the retail savings bond.

Z = Currency Return ( -36% ) ,the currency lost value in that time.

((1+y) x (1+z)) -1

∴ ((1+.07093)x (1-0.36) - 1 (because currency return was negative)

∴ (1.07093 x 0.64)-1

= -31460 X 100

= (-31% return)

That means after 5 years you actually lost 31% (6.2% a year), and this is why investing in sovereign debt in high-risk emerging markets can be risky, because they default through depreciation.

It is also why these rates are soo high at the moment because there needs to be a premium to attract capital, otherwise no body would want to invest in S.A debt. Ultimately it’s you and I that pay the price.

So, although your capital is guaranteed (in nominal terms), the purchasing power of the local currency erodes. (you can buy less)

That is how government defaults on its debt, through currency depreciation.

(2) Inflation

Inflation is directly and indirectly linked to the currency. You get two types of inflation.

(1) Cost-push inflation

(2) Demand-pull inflation

We are experiencing cost-push inflation currently, something we don’t control because we import energy.

Inflation is simply a hidden tax, and on top of the hidden tax you pay, you also have actual tax you pay, which increases the more government borrows. You’ll end up paying no matter what, either through higher interest rates, higher inflation, or currency depreciation - no matter how you look at it, the bill is yours.

(3) Tax

Tax is never kept at the same level, so either you will pay it in it’s hidden form (inflation) or you will be hit with higher taxes - income and VAT.

You are exempt from paying tax on interest if it is below R23 800, anything above that exemption will then be added to your taxable income, based on the marginal tax bracket you find yourself in. All this eats away at your return.

This was one of the reasons why I left S.A, because citizens are being shafted from all fronts, and the states revenue is redirected to non-productive areas in society. Although this happens in all sovereign states, the elites ensure this, but some states are healthier than others.

Just to reiterate:

There are tax Consequences with RSA Retail Savings Bonds

This investment isn’t offered in any Tax Free Savings Account (TFSA), there will be a tax liability attached to this investment. R23,800 is exempt from tax (R34,500 if you over 65 years old) Anything above that then gets added to your taxable income at your marginal tax rate

(4) Opportunity Cost

Locking your money up sounds good, but it may not be the best possible return you could get for the amount of risk you are going to take.

Capital flows to safer havens. i.e. a strengthening dollar with rising rates will attract capital from high-risk markets, unless the risk-premium on offer in those high-risk markets is attractive enough to reflect the risk one must take. (that’s the rate above the risk free rate).

Closing thoughts

Don’t get me wrong,

I’m not saying these risks will materialize, but there are clearly risks to this investment, even though they say it is risk free. Ideally, you would want to lock in 11% and hope the Rand strengthens in those 5 years while your capital is locked, then you’ll benefit handsomely.

If I had to choose between SA Retail Savings bonds or a fixed deposit account at one of the commercial banks, I’d probably go Retail Savings bonds.

Commercial banks (ABSA, FNB, Standard Bank, African Bank, Capitec) don’t guarantee deposits, that means your money isn’t as safe as you think it is. If the bank goes under, your money isn’t insured.

Potentially only up to R100 000 is safe. (Regulation pending)

With that being said,

RSA retail savings bonds can offer a low-risk diversification strategy for those that can’t stomach stock market volatility.

Those with set financial goals may benefit from Retail Savings Bonds

It’s definitely a viable option for those nearing retirement because it currently offers a juicy yield at reasonably ‘low risk’

Stay safe, everyone

See you next week.